![]()

https://www.reviews.com/internet-service-providers/business/ (This article is no longer live)

Professional business services as it should be.

Textor.ca shares over 20 years of experience with remote connectivity, remote working, including Home Internet and WiFi, rural connectivity and telecommunications business cases.

Articles from Textor.ca have been referenced by MarketWatch.com and Reader’s Digest to provide tips and tricks for improving their reader’s experience.

Some definitions for this category: Telecommunications is the exchange of information by electronic means. In the context of what is discussed here, the words broadband, internet, “data communications” or just “communications” may be used.

Two laws govern the growth seen on the internet:

Some current and future use cases needing a large amounts of bandwidth are:

Broadband is now widely recognized as critical infrastructure and with the Coronavirus (COVID-19) internet and related technologies’ adoption rates have soared. The United Nations created the Broadband Commission to further its Millennium Development goals citing Broadband as something that stimulates democracy. Arthur D. Little, Chalmers University of Technology and Ericsson co-authored a report on the Socioeconomic Effects of Broadband Speed citing that doubling broadband speeds for an economy can add 0.3 % to GDP growth.

The world’s journey with Broadband has just begun, let Trevor Textor help you navigate this new world.

![]()

https://www.reviews.com/internet-service-providers/business/ (This article is no longer live)

NBC News published some of my comments; Full article here:

http://www.nbcnews.com/tech/internet/slow-wi-fi-office-exasperating-employees-all-fields-n718731

Did you know that accountants were hesitant to adopt spreadsheet programs like excel? Or that it took us decades to fully adopt trains, automobiles and computers? Do you think these things changed our lives? Of course! How could we conceive where we are today without them? But it took a while for them to gain “steam” (pun intended).

The situation with the Digital Oilfield in North America follows these familiar lines. It is a transformation that I cannot adequately explain since I only know how to build the enabling technology. How it’s going to be used is up to each person acting individually and resulting in a collective connected effect. Sure, I can give some examples or find people who have done this or that. But that’s the tip of the iceberg. The “killer example” is going to be different for every team in an energy company.

The enabling technology for the Digital Oilfield is called a “Connected Field”. It takes the Oilfield improvement areas listed below and binds them together. It’s the enablement of seamless intercommunication and coordination that truly leverages a Digital Oilfield. Without it, it’s an Oilfield that uses new Oilfield technology – not the exciting “Digital Oilfield” that truly propels the energy business to the next level.

There are so many ways to get a Connected Field wrong for a Digital Oilfield. Even with the right telecom vendors, it’s so easy to say “we don’t need QoS (Quality of Service)” – simply because the decision maker doesn’t know what it is. The fallacy is that there is a belief we already have a Digital Oilfield. There are already real world examples of a true Digital Oilfield using a Connected Field. And they are all in the Middle East; lowering their costs and increasing their supply. I cover a real world example later, so it will be easy to see the difference.

But let’s go back to the beginning. What is a “Digital Oilfield”? The concept was first presented in the seminal study: “The Digital Oilfield of the Future: Enabling Next Generation Reservoir Performance”, IHS Cambridge Energy Research Associates, Inc., 2003.

A Digital Oilfield makes the following improvements to the Oil & Gas business – and a Connected Field enables most of them; that is, you need a connected field to truly leverage the benefit to the full extent.

So what is a “connected field”? It is a data communications system that has these characteristics:

Let’s examine what is not a connected field:

And of course, I hear all the skeptics. So what does a Digital Oilfield do in practice? Here’s an example:

Petroleum Development Oman (PDO)

What does the Connected Field network look like for PDO?

As of the end of 2013, Petroleum Development Oman field has:

Compare this to a field of that size in North America; there are maybe 10 cellular base stations covering the entire thing. Everything overloaded to the point that it does not work that well (e.g. “worse than dialup” is what I frequently hear).

Together the Connected Field collects 36 times more data enabling more accurate and improved decisions. It delivers 4 Mbps anywhere within the field of coverage (compared to less than 300kbps in some fields available today). You can drive around in a truck all day long and everything just works.

No messing with devices, changing networks, etc. Need to talk to the engineer in head office and start a video chat about a valve to show him/her the valve? Done! No problems. Want to implement an intelligent video system to monitor the flare stack, look for pipeline leaks, identify personnel not wearing PPE, etc.? Want a “mobile worker”? (Please do not confuse it with a “mobile OS” which is simply an operating system built to enable mobile workers that have a network.) With a Connected Field, you just do it! No need to price in a brand new network to enable the business case.

The cost of all this? Less than 1% of the total injected capital into a greenfield area. And if a true connected field is implemented that is multi-use and multi-team capable, the expenditure is less than what they spend today.

Despite the impressive track record how many Digital Oilfields are there in North America? None. Some are close with partial implementations but it’s localised and not well championed at the executive and board levels. How many in the Middle East? Quite a few. Middle East operations have the direct support of the board of directors/families and executives. Would this situation have any bearing on the current supply / demand and geopolitical climate? Hmm….

Even in today’s poor commodity climate – many cost savings projects with a 2-3 year payback (50% IRR) period go undone. If you don’t recall what the payback period or IRR is, please see my post:

“Who likes making money? Payback, RoI, IRR explained…” https://www.textor.ca/2016/03/who-likes-making-money-payback-roi-irr-explained/

There are two things to note about cost savings projects. They typically:

Based on this, a company should always do periodic cost reduction projects – in a good or bad commodity environment since it increases the profit margin in good times and allows a company to survive longer than its competitors in bad times (and survivors always do the best in the long run).

Correct me if I’m wrong… but from what I recall from what Oil and Gas executives have told me, any Oil & Gas project with over a 30% IRR is always approved. However, it’s been entirely up-hill trying to convince Oil & Gas to approve these projects.

I’m going out on a limb here though…. Maybe the reason why is that they are connectivity (telecommunications) projects for rural areas? Connectivity usually falls within the IT department and from my interviews with CIOs, there is little focus on connectivity costs. That is, they feel that connectivity is not really an IT role but it gets lumped into IT so they suffer through it. I agree with them – IT is getting dumped on due to poor understanding of connectivity at the leadership levels. After over a decade doing rural connectivity, I believe that connectivity should be an engineering role and connectivity commissioning and operations should be in IT. This arrangement makes the basic procurement management build (engineering) vs rent (off the shelf) calculation possible. Let’s face it, IT is not engineering. IT is only going to rent. But most of the time, it is more effective to build in rural Oil & Gas locations.

The final nail in the coffin for this whole scenario is that connectivity is critical infrastructure (like water, electricity). This basically means you can’t do things that are expected of a company operating in the current economic environment without it. I have had to deliver the bad news to hundreds of promising Oil & Gas projects because the current network they have cannot support anything but the basics (e.g. kilobit per second SCADA – or what I call “tin can on a string” data). The cost of this one fact alone is colossal. I explain more about this in my presentation “Understanding the Remote Field Data Communications Challenge”

http://www.slideshare.net/TrevorTextor/understanding-the-remote-field-data-communications-challenge

Anyone care to chime in? Anybody have an Oil and Gas producer or midstream company (operates rurally with large footprint) who does not focus on connectivity and would love to save money?

Great to see jurisdictions taking action with the digital divide economic problem: this is clearly a data communications (broadband) delivery issue or we wouldn’t need a United Nations Broadband Commission to educate countries about this. Mexican government’s digital divide initiative is delivering 1500 base stations to service 64,000 sqr km (25,000 sqr miles) using Redline’s product. Redline won the bid by demonstrating that Redline’s product needed less total base stations and has better longevity. A total cost of ownership (TCO) calculation. Job well done! http://yourcommunicationnews.com/redline+communications+awarded+%241.7m+contract+for+major+wireless+network+in+mexico_129241.html

Karin Williams shares her founding story. Karin has been my primary and enduring mentor since starting my own business and her wisdom has rung true more times than I can count. Her brand of honest, respectful business conduct I truly cherish as I have found that it’s in less abundance than I had hoped. Congratulations Karin for navigating RioTel through 17 years. A true accomplishment!

https://www.linkedin.com/pulse/my-founder-story-circa-1999-karin-williams

“Broadband Internet – The “Railroad” of Our Era”, a general view of broadband internet, followed by:

“Understanding the Remote Field Data Communications Challenge”, rural telecom for Oil & Gas “in a nutshell”.

Non-IEEE members are welcome. Registration opens at 5:15pm, presentations start at 6pm.

More about the presentation here:

The big telecom companies have been hiding behind excuses for years but those excuses are no longer holding water. With email systems doing it regularly, we know better; These excuses do not hold water anymore.

Consumers Union has taken a stand and is making progress. An update email from Consumers Union USA dated Dec 22, 2015:

“Last year at this time, hardly anyone believed robocalls could be stopped.

The Do Not Call list wasn’t working. Scammers quickly disappeared and reopened shop before the cops could find them. And your phone company just ignored you when you asked for help.

But together, with you, we changed all that.

After our campaign launched in February, the FCC and nearly every state Attorney General followed Consumers Union’s lead and told the phone companies to block these calls. Members of Congress introduced legislation. And presidential candidates even talk about this on the campaign trail.

Now, we are bringing Verizon, AT&T and Century Link to the negotiating table in the New Year. We will be representing your demands for free tools to block robocalls before they reach your phone – and we won’t back down!

…

When we started this campaign, everyone thought we were nuts. It was such a perplexing problem that regulators, who tried for years to stop robocalls, even held a contest looking for solutions. And the giant phone companies didn’t want to act, hiding behind the claim that they didn’t have the legal authority to block these calls.

But you told us robocalls were ruining your quality of life. And for others, your bank accounts. Some $350 million is stolen each year from consumers – mainly the elderly who take these calls and are quickly duped.

It’s been a long haul, but together we’ve made huge progress. Once thought an impossible problem, our research has found several solutions that will dramatically reduce robocalls. Now we’re headed to the major phone companies demanding they implement these solutions for you!

…

Thank you,

Tim Marvin, Consumers Union

Policy and Action from Consumer Reports”

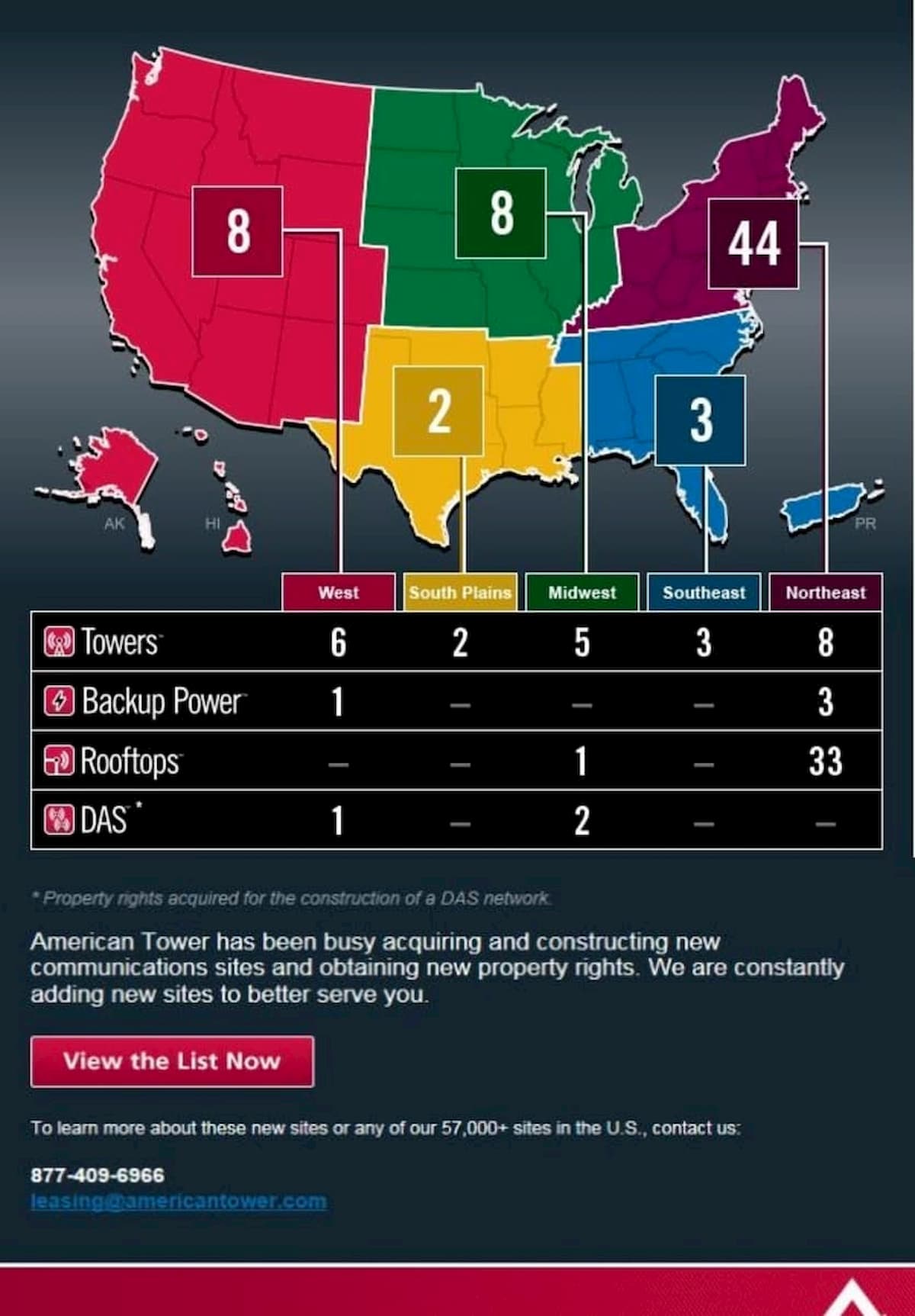

When I mention “TowerCo” (Tower Companies), real estate companies that are like an apartment building landlord… but for towers, I see the confusion in people’s eyes. Essentially, the tenants (renters) are antennas that get mounted to the tower (apartment building). What’s the best way to visualize what one looks like? Well, just look at their advertising – they have towers for rent! Here’s an advertisement from American Tower showing that they have acquired new towers in the following USA geographic locations.

(click to enlarge)

The TowerCo industry itself comprises many companies across the globe. According to the industry’s journal TowerXchange, TowerCos already own 2/3rds of the world’s 3 Million towers. In the USA TowerCos own ~61% of the ~270K towers. In Canada, that figure is less than 5%.

TowerCo ownership, or companies that are exclusively real estate (do not sell telecom services), are a key indicator for broadband costs (e.g. cell phone data plans). This is because they offer a business model that promotes sharing and reduces costs. The reader may learn more about how the TowerCo business model reduces costs on my slideshare presentation entitled “Broadband Internet – The ‘Railroad of Our Era'”.

In the USA the top 3 tower companies listed on the New York Stock Exchange are:

All three operate as “Real Estate Investment Trusts” (REITs), further confirming that they are real estate companies. Collectively they own, lease and manage 95,000 towers and are worth $69 Billion. One of these top 3 companies, SBA, has moved into Canada with a subsidiary called SBA Canada. (@ early 2014) The other major TowerCo in Canada is Turris Corp.

I’m including text from the podcast “Tower Talks with Inside Towers: #15 – TowerXchange CEO Kieron Osmotherly” (@9:17) which accurately summarizes the TowerCo strategy from the perspective of a mobile network operator (examples are Telus, Bell, AT&T, Verizon, etc) and provides some metrics on the performance of this business strategy.

We pickup in the podcast where Kieron is talking about the common fundamentals of the Tower market: “… [A] telecom tower on a mobile network operator’s balance sheet is a depreciating asset built to serve the needs of one customer. You take that tower and you put it on a Tower company’s balance sheet and it becomes a potential source of long term recurring revenue from multiple credit worthy tenants.

We’re correcting a flaw in the original design of wireless communications which created this overlapping infrastructure. And we’re correcting that to a more efficient collocation driven model. The capital markets recognize that. It’s reflected in the valuation performance of tower companies. It aggregates up to a $330 Billion dollar global infrastructure asset class which is out-performing most relevant comparisons.

As we mentioned before between them the tower companies now have 69% of the world’s invest-able assets which is a pretty good proportion. Most tower companies stick to that blueprint.

There is significant variation when you look at the difference between a pure play independent tower company like American Tower, SBA, Cellnex, HBS. These guys are fantastic at shareholder value creation and generating efficiencies. They typically trade at EBITA margins between 60-80% valued 15-25x.

And then we’ve got a relatively recent variant on the business model which we call the operator-led tower company [TowerCo]…. It’s at least 50.01% owned by the original parent mobile network operator(s). In comparison, to a pure play independent tower company [TowerCo] you often see slightly lower EBITA margins of perhaps 40-60%. And valuations of 10-15x are still significantly greater than the valuations of mobile network operators.

I think we’ve arrived at the day and age where pretty much everyone understands that a tower that’s trapped on a mobile network operator’s balance sheet is uh, it’s difficult to defend that position to shareholders these days. Whether you’re going to carve it out or sell it, it should be shared.”

An avid writer, Trevor Textor has been quoted by Reader’s Digest, NBC News, Reviews.com and MarketWatch.com. As a freelancer Trevor has moved towers off of an Oil & Gas company’s balance sheet in a sale and leaseback deal to a TowerCo. Ask Trevor if he can help: https://www.textor.ca/contactme/

LocalInternetService.com interviewed Trevor Textor for input and editorial help with the ISP section.

http://www.localinternetservice.com/resources/internet-throttling

The article focuses on: