Trevor Textor’s Blog Posts about Investing. Trevor Textor is highly versed in Personal Finance and coaches in the investment strategy called “The Single Best Investment” (a variation of the

“Dividend Achievers” strategy).

“All of these early retirement articles are the same. They all say things like, “Make it a goal”, “Track your expenses”, “Establish a system.” Blah. Blah. Blah. But none of these things are the actual reason for how they retired early. Because the actual reason is either (1) earning a high income or (2) having an absurdly low level of spending, or both.”

….

As a public service, the article includes more realistic headlines for retiring early, “Wanna retire at 27? Marry rich” and “Foregoing Procreation, Living Like a Hermit, and 4 Other Ways to Retire in Your 30s”.”

Let’s boil this down quickly – if you’re a Canadian and you do what everyone else does with your savings and investments you will never get ahead. As I explain why let’s look at what is happening in the USA. The USA is moving to execute a fiduciary duty on its financial advisors that includes a “conflict of interest” rule. The “conflict of interest” referred to is the fact that any financial advisor that is not fee-only receives a commission on what they advise their clients to do. In Canada, this is most advisors encountered by Canadians.

As Barrie McKenna writes, commissions put enormous pressure on the advisor to make sales volume targets and even discovers that because of this “…[j]ust to break even, investors typically must generate annual returns of 5 to 8 per cent to cover fees, commissions, trading costs and inflation…” an estimate from Victor Therrien, a mutual fund industry veteran and former executive vice-president of Brandes Investment Partners.

On a similar “conflict of interest” rule move in Canada there is silence. Indeed David Di Paolo and Kara Beitel, partners of Borden Ladner Gervais LLP counsel against it saying “A blanket imposition of a fiduciary standard would ignore the realities of many advisor-client relationships.” In their article they almost completely ignore the “conflict of interest” elephant in the room.

As one of the Canada Post unions moves to disrupt the Canadian Postal system, I think now is a great time to discuss Defined Benefit (DB) Pensions which is the main issue for the union. Most private companies have moved to a Defined Contribution (DC) system; why? DB pensions are eerily similar to Ponzi schemes moving some to call DB pensions “legalized Ponzi schemes” (where the taxpayer bails out the “last in” pensioner and the company offering the DB pension goes into bankruptcy). FiduciaryNews.com published an enlightening article on Aug 28, 2014 that dives deeper into this question:

What do you think? Do you think it’s fair for a small group of people’s lifestyle to be funded by the Canadian Taxpayer?

I personally do not believe this is fair, and in 1999 when I was offered the choice between DB or DC pension (the last year DB was offered at the company I worked at), I chose a DC pension. In all honesty, I would rather no pension* as I have since learned of a way to not depend on any pension system which I talk about here:

This above mentioned method is both responsible to other people (tax payers) and has the upside benefit of enabling more money to people in retirement than an equivalent DB pension (assuming the person starts the strategy when they enter the workforce and let it run for 25+ years like a DB pension would do). The method has been stress tested by people who have lived on the poverty line and still were able to use the strategy successfully.

* Pensions in the truest sense are government legislated rules to force people to save for retirement; the underlying assumption is that people are not capable of being responsible for their own future. Therefore, the government needs to step in with rules so people don’t blow their own foot off and leave the government and other people with a huge liability as people age.

You know that feeling, “I’m not saving enough. If I could only win the lottery…” That pressure we put on ourselves is unnecessary and in fact, the system is rigged against us. The financial system itself is intent first on accumulating money, second (or even third) is to make a profit for you.

How The Financial System Delays Retirement

Long-time investment advisor Adam O’Dell spills the beans on his former employers in an article entitled “Why I quit My job as a Financial Advisor” with “…I was expected to toe the company line and only recommend strategies and investments that were “pre-approved,”… Most of the time, that advice centered on “traditional” investment tenets: dollar-cost averaging (read: buying a little more each month), buy-and-hold (err, more like “buy-and-hope!”), asset allocation (but just long stocks and bonds). The odd thing, to me, was that our recommendations in 2008 [, a year of financial crisis,] weren’t all that different from all the years prior. The state of the market seemed to make no difference.”

We spend a lot of money on advisors and money managers. The trick is that they hide the cost in a low sounding management expense ratio (MER) of typically 1-2.5%. So how much is that really? I sat down and figured it out. Because it’s a percentage, we need to consider large sums of money, since the traditional retirement strategy everyone expects is big pot of gold and then taking a few coins out each month to live on. So I started with $100,000 but a more likely figure is several million. Drumroll please!! It costs us around $400-1400/hr (or more!) to pay for these funds and the time it takes to manage the money for you. Most people think twice about paying a professional this much money. Here is a spreadsheet which you can play with yourself. Try changing the number from $100,000 to $1,000,000 or whatever suits your fancy. Click here to access the spreadsheet. This then is why the universal recommendation is to only use a fee-only financial planner. One that doesn’t make commissions or is motivated to put you in funds that charge an MER.

Further digging into the spreadsheet mentioned, it tells us why that Mutual Fund or Exchange Traded Fund (ETF) basically treads water. Take that traditional retirement model; the big pot of gold. How many coins can we take out of it each year? Called “a safe withdrawal rate” my research indicates a reasonable amount is 2%. Remember, the fund is charging you the MER in retirement and also in situations where the fund loses money. So add the MER and the safe withdrawal rate together and you have a significant negative trend against building wealth.

The Single Best Investment (AKA “Dividend Achievers”)

There is a better way…. Something I stumbled on to. It has a significant history of success dating right back to the start of the stock exchange in 1602. Mr. Lowell Miller introduced the concept to me in his book, now a free PDF online, called “The Single Best Investment: Creating Wealth with Dividend Growth.” (It is also on amazon if you want to pay for the e-book or buy an old paper copy. Also, there are copies at most public libraries.)

Single Best Investment has also been called the “dividend achievers” strategy and is one of the few (only?) proven long term buy and hold strategies that work. What is it? Basically it is an investment in stocks that have raised their dividend every year. Meaning the investment is not for the dividend itself but the dividend growth rate. Click here for more on “dividend achievers”.

How the Single Best Investment Works

It works because it does two critical things:

eliminates financial fees

focuses money in companies that stay healthy with very low risk of long term downside

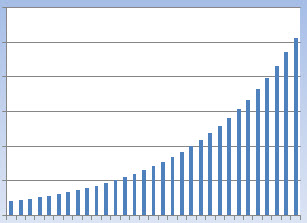

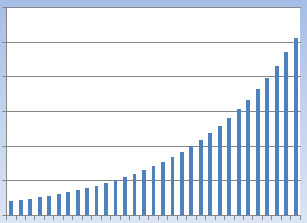

Because it is based on a growth rate for dividends, there is a “hockey stick” compounding growth graph. (You can learn more about “Payback, RoI, IRR” by clicking here.) That also means it takes time and is not a “get rich quick” (GRQ) scheme. Other characteristics of this strategy are:

Simple, minimal maintenance strategy

Focuses on key factors important to personal financial situations: cash flow, safety

Still grows if cash flow not reinvested

Cash flow increases through retirement

Can eliminate the need to continuously save for retirement

Supports “rewirement”

Qualifies for debt interest deductibility (an advanced tax strategy)

Congratulations! You Care About Your Money!

If you made it the bottom of this article, congratulations. You are one of the few people who cares that your money makes money. Not many people do. North American society has all sorts of funny money myths, and collectively we subconsciously do not think we deserve it. Have you ever tried to talk to a fellow North American about money? You’ll see.

So what do I do? I have documented my experience and tools to help bootstrap people. Most people tell me they “don’t have the skills to invest themselves” but most people already do tasks many times more complex than investing. To list the required skills a person needs to know how to read, multiply, divide and handle percentages.

Next Steps

I offer a 3 hour introductory course (contact me here) and pay as you go coaching for people not inclined to read the book and do-it-themselves. To date, no one has ever needed more than 4 hours total. It is that easy. The strategy requires some time to setup, but then it’s “set it and (mostly) forget it”; just like buy and hold should be. For those who do not have much seed money and want to know what tools are available to help accelerate their progress, I offer an additional advanced course. If you think investing and saving is way beyond your lifestyle, consider that people making poverty line incomes have successfully used this strategy. That’s one of the many money myths.

About my involvement as a coach: I don’t make enough money from this for it to be anything but a hobby that makes a little money. The other reason I charge is because we can’t have a contract that places the responsibility for investing on the investor without doing so. The reason I coach is because I believe it benefits people. What I don’t do is provide motivation for conducting the strategy although I do discuss the psychological hurdles as part of the course. The psychology and the motivation are the hard part and finding tools for overcoming that comes from countless motivational materials available at any book store or library.

What’s a payback period? How does it compare to Return on Investment and Internal Rate of Return?

A good question. A payback period is the time it takes for the benefit of a project (cost savings or increased revenue) to pay back the initial capital of the project. For example, you have a project that costs $2,000 and takes a year to complete. After it is completed it saves you $1,000 yearly (no end date in this example). That means the project will take 2 years to be paid back after the project’s completion ($2000/($1000/year) = 2).

So how does this compare to Return on Investment (RoI)? Simple ROI = (Gains or savings – investment costs) / Investment Costs. It does not take time into account. For instance, with the above example, after 3 years the RoI is ($3000-$2000)/$2000 = 50% but after 10 years the ROI is ($10,000-$2,000)/$2000 = 400% – so the RoI keeps escalating toward infinity over time… not very useful. Internal Rate of Return (IRR) however, is!

IRR is a compounding rate of return. I won’t go into the calculation but the above example has a ~50% IRR. Since it’s compounding we can use the “rule of 72” to figure out what this really means. The rule of 72 tells us how many years it takes to double the cumulative benefit. So 72/50= 1.44 years. So at 1.44 years the gain/savings is $1,440. At 2.88 years it is $2,880. At year 5.76 it is $5,760. And so on…

At left is the compounding “hockey stick” graph. This is the hockey stick graph for my “rewirement” strategy (9% compounded yearly) – coincidently this is the same strategy that I coach about. It’s the only buy and hold strategy that works in an up or down market, has over 150 years of market data behind it, is the laziest DIY strategy and that most anyone can do (assuming you understand addition, subtraction, multiplication and division).

A slow start initially and then ZOOM! upward. Compounding in action!

If you are interested in this strategy, I read about it in a book that is freely downloadable on the internet or you can get the book from a library or a used bookstore:

I liked reading it but many people tell me it’s boring… I guess I get excited enough about making money to read it through. What I coach in is the “how to” part; complementary to the book (or for people who don’t want to read it and want the summary). People are fully coached in approximately 2-4 hours depending on the person (2 hour basic course plus additional time as needed). However, I love to support “do it yourselfers”, and if you are one, you can probably figure out the “how to” part using Mr. Miller’s book with some invested time. However, if you want a jump start, please let me know! I discuss the strategy more here: https://www.textor.ca/single-best-investment-doomed-retirement-feeling/

I actually asked Mr. Miller if it was ok if I coached people using his book as the basis. He said “sure!”. You have to wonder… this strategy 100% works; always! Mr. Miller has published two versions of his book over the last decade+ before finally allowing people to read it for free on the internet. Clearly, people aren’t using it en masse. Every single person I have coached says “Why doesn’t everyone do this? It’s so easy!” and “I wish I had done this X years earlier.” No one has ever told me “this is a waste of time”. Mr. Miller is a fund manager – which the book basically discourages using. And even after Mr. Miller tells his clients not to use him and how to do it themselves, they still want Mr. Miller to manage their money. Such a strange world we live in!

Note: I owe recognizing the strength of this strategy as I read that book to my knowledge of IRR and payback periods. Good things to know!

By the CRTC mandating that telecom companies must share their passive broadband infrastructure might mean that Canada is moving toward an OAN. That means companies might actually need to show a return on investment for their passive infrastructure assets (fiber, conduit, towers) rather than using them to block competition. I’m all for the Telecom companies making a profit (I’m a shareholder of many of them) but I’d rather they do it on the service side in open, honest competition. We know from experience that competition drives companies to be innovative. I would like all the Telecom companies I own to be around for a long, long time and the “we’ve always done it this way” (no innovation) is going to kill them.

The majority of effective broadband rural last mile is terrestrial wireless and that means communications towers are really important. The tower “real estate” industry is complicated – follow the link to see TowerXchange’s Value Chain illustration. What is this emerging real estate industry? Instead of people as tenants, the tenants are radios. The top 3 tower companies listed on the New York Stock Exchange collectively own, lease, manage 95,000 towers and are worth $69 Billion. One of these top 3 companies, SBA, has moved into Canada.

This podcast is an excellent example of how collective human psychology can take down the global financial system. From a school lunch room we hear an eerily similar story to that of Tulipomania; widely considered the first economic bubble in 1637 when a single tulip bulb sold for +10x the annual income of a skilled craftsman.

Pension funds are a great place for corruption. Place the management of a lot of money into the hands of a few people and let human nature take its course. This podcast takes an excellent look into the world of pensions.

Project Managers and Business Analysts have roles that blur together and are often confusing. So what is it that a BA does?

“…a Project Manager will deliver, on time, on budget and in scope, the perfect set of concrete shoes; but without a Project Manager, a Business Analyst might never deliver at all. … If [an] outcome doesn’t provide value for an organization we have concrete shoes. And here is our sweet spot for business analysis as a discipline. Yes I said discipline. It is time to stop thinking about business analysis as a role, title or profession. Business analysis is a disciplined way of approaching any decision so as to provide value to further an organization’s objectives. The objectives of an organization are fulfilled through its strategy. …”