TowerCo

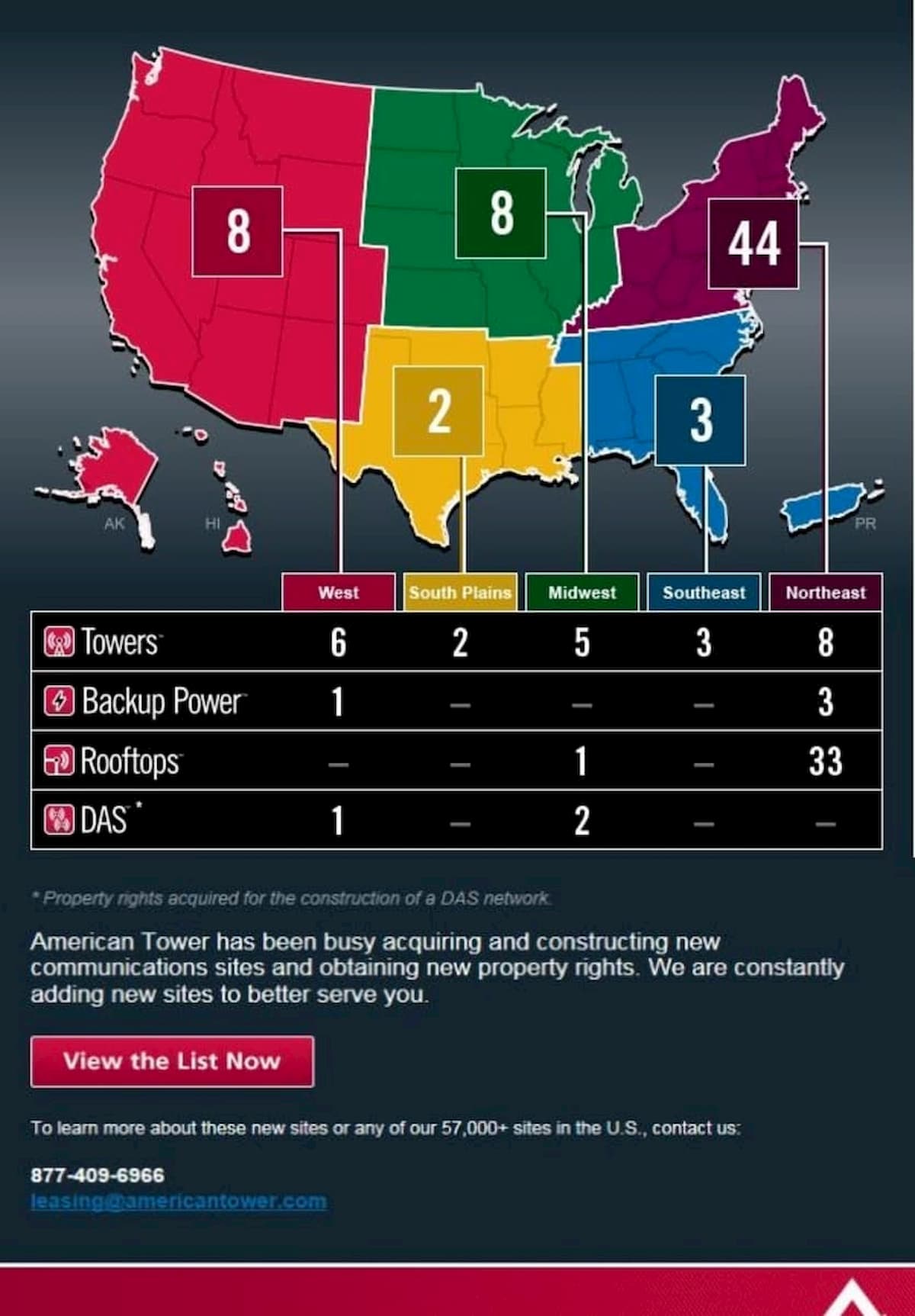

When I mention “TowerCo” (Tower Companies), real estate companies that are like an apartment building landlord… but for towers, I see the confusion in people’s eyes. Essentially, the tenants (renters) are antennas that get mounted to the tower (apartment building). What’s the best way to visualize what one looks like? Well, just look at their advertising – they have towers for rent! Here’s an advertisement from American Tower showing that they have acquired new towers in the following USA geographic locations.

(click to enlarge)

The TowerCo industry itself comprises many companies across the globe. According to the industry’s journal TowerXchange, TowerCos already own 2/3rds of the world’s 3 Million towers. In the USA TowerCos own ~61% of the ~270K towers. In Canada, that figure is less than 5%.

TowerCo ownership, or companies that are exclusively real estate (do not sell telecom services), are a key indicator for broadband costs (e.g. cell phone data plans). This is because they offer a business model that promotes sharing and reduces costs. The reader may learn more about how the TowerCo business model reduces costs on my slideshare presentation entitled “Broadband Internet – The ‘Railroad of Our Era'”.

TowerCo Market

In the USA the top 3 tower companies listed on the New York Stock Exchange are:

- SBA Communications

- American Tower

- Crown Castle

All three operate as “Real Estate Investment Trusts” (REITs), further confirming that they are real estate companies. Collectively they own, lease and manage 95,000 towers and are worth $69 Billion. One of these top 3 companies, SBA, has moved into Canada with a subsidiary called SBA Canada. (@ early 2014) The other major TowerCo in Canada is Turris Corp.

TowerCo Strategy

I’m including text from the podcast “Tower Talks with Inside Towers: #15 – TowerXchange CEO Kieron Osmotherly” (@9:17) which accurately summarizes the TowerCo strategy from the perspective of a mobile network operator (examples are Telus, Bell, AT&T, Verizon, etc) and provides some metrics on the performance of this business strategy.

We pickup in the podcast where Kieron is talking about the common fundamentals of the Tower market: “… [A] telecom tower on a mobile network operator’s balance sheet is a depreciating asset built to serve the needs of one customer. You take that tower and you put it on a Tower company’s balance sheet and it becomes a potential source of long term recurring revenue from multiple credit worthy tenants.

We’re correcting a flaw in the original design of wireless communications which created this overlapping infrastructure. And we’re correcting that to a more efficient collocation driven model. The capital markets recognize that. It’s reflected in the valuation performance of tower companies. It aggregates up to a $330 Billion dollar global infrastructure asset class which is out-performing most relevant comparisons.

TowerCo Investment

As we mentioned before between them the tower companies now have 69% of the world’s invest-able assets which is a pretty good proportion. Most tower companies stick to that blueprint.

There is significant variation when you look at the difference between a pure play independent tower company like American Tower, SBA, Cellnex, HBS. These guys are fantastic at shareholder value creation and generating efficiencies. They typically trade at EBITA margins between 60-80% valued 15-25x.

And then we’ve got a relatively recent variant on the business model which we call the operator-led tower company [TowerCo]…. It’s at least 50.01% owned by the original parent mobile network operator(s). In comparison, to a pure play independent tower company [TowerCo] you often see slightly lower EBITA margins of perhaps 40-60%. And valuations of 10-15x are still significantly greater than the valuations of mobile network operators.

I think we’ve arrived at the day and age where pretty much everyone understands that a tower that’s trapped on a mobile network operator’s balance sheet is uh, it’s difficult to defend that position to shareholders these days. Whether you’re going to carve it out or sell it, it should be shared.”

About the Author

An avid writer, Trevor Textor has been quoted by Reader’s Digest, NBC News, Reviews.com and MarketWatch.com. As a freelancer Trevor has moved towers off of an Oil & Gas company’s balance sheet in a sale and leaseback deal to a TowerCo. Ask Trevor if he can help: https://www.textor.ca/contactme/

One Reply to “What does a TowerCo “look like”? (introduction to Real Estate for Telecom)”